Unlock Savings: A Simple Guide to Lowering Your Credit Card Interest Rate

Hey there, savvy spender! Let's face it, credit cards can be a double-edged sword. They offer convenience, rewards, and can be lifesavers in a pinch. But those interest rates? Ouch! They can sneak up on you and quickly turn that emergency purchase into a long-term financial burden. Ever feel like you're just treading water, making payments but barely making a dent in the principal? You're not alone! Millions of people are in the same boat, battling high interest rates that eat away at their hard-earned cash. Think of it this way: you’re basically paying extra for the privilege of using the card. It's like ordering a pizza and then having to pay an extra "convenience fee" on top of the delivery charge and the tip – infuriating, right? The good news is, you don't have to resign yourself to paying exorbitant interest fees forever. You have more power than you think, and you can actually negotiate a lower credit card interest rate. Sounds too good to be true? Well, stick with us, because we're about to reveal the secrets to sweet-talking your way to savings. Prepare to learn how to take control of your finances and say goodbye to unnecessary interest payments. Are you ready to unlock the secrets? Let's dive in!

How to Negotiate Lower Credit Card Interest Rates

Let's be honest, the thought of calling your credit card company and asking for a lower interest rate might feel a little intimidating. It's easy to imagine being met with resistance, rejection, or even worse, a condescending tone. But trust us, friends, it's absolutely worth a shot. Negotiating a lower rate can save you hundreds, even thousands, of dollars in the long run. So, how do you approach this delicate dance? Fear not! We've got you covered with a step-by-step guide to help you navigate the negotiation process like a pro.

•Know Your Worth:Check Your Credit Score.

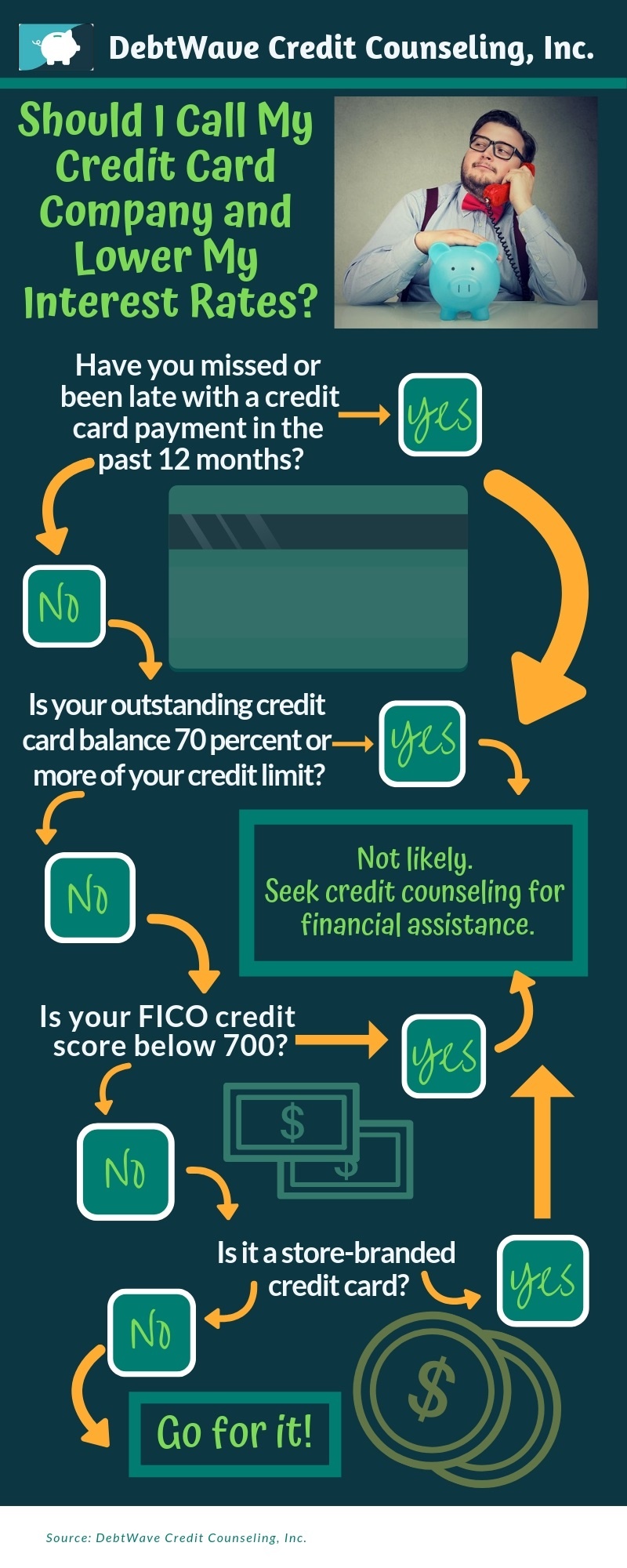

Before you even think about picking up the phone, it's crucial to understand your credit score. Your credit score is a three-digit number that essentially tells lenders how trustworthy you are as a borrower. A higher score means you're more likely to repay your debts on time, making you a less risky customer. Credit card companies often reward lower-risk customers with lower interest rates. You can typically check your credit score for free through your bank, credit card issuer, or websites like Credit Karma or Experian. Understanding your credit score is the first step in showing them that you're serious.

If your score is in the "good" to "excellent" range, you're in a strong position to negotiate. If it's lower than you'd like, don't despair! You can still try to negotiate, but be prepared to address any concerns the credit card company might have. Be ready to explain how you're actively working to improve your score, such as paying down other debts or correcting any errors on your credit report.

Imagine your credit score as your financial resume. You want to make sure it's polished and highlights your best qualities. A good credit score isn't just about bragging rights; it's your ticket to lower interest rates and other financial benefits.

•Do Your Homework:Research Current Interest Rate Trends.

Knowledge is power, and that's especially true when it comes to negotiating. Before you call your credit card company, take some time to research the average interest rates currently being offered for similar cards. Websites like Bankrate, Nerd Wallet, and Credit Cards.com provide up-to-date information on interest rate trends and can help you get a sense of what a reasonable rate would be for someone with your credit profile. It's like scouting out the competition before a big game. You need to know what the playing field looks like so you can develop a winning strategy.

Knowing the average interest rate will give you a benchmark to aim for and will also demonstrate to the credit card company that you've done your research and aren't just pulling numbers out of thin air. You can say something like, "I've noticed that other credit card companies are offering rates as low as X% for customers with similar credit scores. I'm hoping you can match that." This shows them that you're informed and serious about getting a better deal.

•Prepare Your Pitch:Highlight Your Loyalty and Payment History.

Now comes the fun part: crafting your negotiation pitch. This is your opportunity to shine and convince the credit card company that you're a valuable customer worth keeping. Focus on your positive attributes, such as your long-standing loyalty to the company, your consistent on-time payment history, and your overall responsible credit behavior. Think of it as your elevator pitch – you need to make a compelling case in a short amount of time.

Prepare specific examples to support your claims. For instance, you could say, "I've been a loyal cardholder for five years and have never missed a payment." Or, "I consistently use my card for everyday purchases and always pay my balance in full or make more than the minimum payment." These details demonstrate that you're a reliable and profitable customer, making you more likely to get a favorable response.

Remember, you're not just asking for a favor; you're making a business case. You're essentially saying, "I'm a good customer, and I deserve a better rate."

•Make the Call:Be Polite, Confident, and Persistent.

Alright, it's showtime! Take a deep breath, dial the credit card company's customer service number, and prepare to unleash your negotiation skills. The key here is to remain polite, confident, and persistent throughout the conversation. Remember, the person on the other end of the line is just doing their job, so treat them with respect, even if you don't immediately get the answer you're hoping for. It's like approaching a salesperson – you want to be friendly and approachable, but also firm in your needs and expectations.

Start by clearly stating your request. For example, you could say, "I'm calling to request a lower interest rate on my credit card. I've been a loyal customer for X years and have always made my payments on time." Then, present your research on current interest rate trends and highlight your positive credit history. Be prepared to answer any questions they may have and to address any concerns they raise.

If the first representative you speak with isn't willing to budge, don't give up! Politely ask to speak with a supervisor or someone who has the authority to make decisions on interest rates. Sometimes, it just takes talking to the right person to get the outcome you're looking for. Remember, persistence pays off!

•Be Prepared to Negotiate:Offer Alternatives and Compromises.

Negotiation is a two-way street, so be prepared to offer alternatives and compromises if necessary. The credit card company might not be willing to give you the exact interest rate you're hoping for, but they might be willing to meet you halfway. Think of it as haggling at a flea market – you might not get the item for the price you initially wanted, but you can often negotiate a mutually agreeable price.

For example, you could suggest that you're willing to transfer your balance to another card with a lower interest rate if they can't offer you a competitive rate. This shows them that you're serious about finding a better deal and that they risk losing you as a customer. Alternatively, you could ask if they offer any balance transfer promotions or other incentives that could help you save money on interest.

The key is to be flexible and creative. The more options you have on the table, the more likely you are to reach a successful outcome.

•Know When to Walk Away:Consider Balance Transfers or Other Options.

Sometimes, despite your best efforts, the credit card company simply won't budge. They might claim that they can't lower your interest rate due to market conditions or internal policies. In that case, it's important to know when to walk away and explore other options. Don't feel like you're stuck with a high interest rate forever. It's like realizing that a car dealership isn't offering you a fair price – you're better off walking away and finding a better deal elsewhere.

One option is to consider transferring your balance to a credit card with a lower introductory interest rate. Many credit card companies offer balance transfer promotions that can save you a significant amount of money on interest, at least for a limited time. Just be sure to read the fine print and understand any fees or restrictions that may apply. Another option is to explore personal loans, which often have lower interest rates than credit cards, especially if you have good credit.

Remember, you're in control of your finances. Don't be afraid to shop around and find the best options for your individual needs.

•Document Everything:Keep Records of Your Conversations and Agreements.

Finally, it's crucial to document everything throughout the negotiation process. Keep a record of the date and time of your calls, the name of the representative you spoke with, and the details of your conversations. If you reach an agreement on a lower interest rate, make sure to get it in writing. This will protect you in case there are any discrepancies or misunderstandings down the road. Think of it as creating a paper trail – you want to have evidence of your agreement in case you need to refer back to it later.

You can also send a follow-up email to the credit card company confirming the details of your agreement. This provides an extra layer of protection and ensures that everyone is on the same page. By keeping thorough records, you can avoid potential headaches and ensure that you get the savings you've negotiated.

By following these steps, you'll be well-equipped to negotiate a lower credit card interest rate and save yourself some serious money. Remember, it's all about being prepared, confident, and persistent. Good luck, friends, and happy saving!

Frequently Asked Questions

Let's tackle some common questions about negotiating lower credit card interest rates to make sure you're fully prepared.

•Q:Will asking for a lower interest rate hurt my credit score?•

A: Generally, simply asking for a lower interest rate will not directly hurt your credit score. The credit card company might do a "soft inquiry" to review your account, but this doesn't impact your score. However, if you apply for a new credit card to transfer your balance, that new application can result in a "hard inquiry," which might slightly lower your score temporarily.

•Q:How often can I negotiate my credit card interest rate?•

A: There's no hard and fast rule, but it's generally a good idea to wait at least six months between requests. If your credit score has improved significantly or market interest rates have changed, you might have a stronger case for negotiating sooner.

•Q:What if I have a poor credit score? Can I still negotiate?•

A: It's definitely more challenging, but not impossible. Focus on demonstrating that you're working to improve your credit, highlight any positive payment history, and emphasize your loyalty as a customer. You might also consider secured credit cards or credit-building loans to improve your score before negotiating.

•Q:The representative said they can't lower my interest rate. What should I do?•

A: Don't give up immediately! Ask to speak with a supervisor or someone with more authority. If that doesn't work, consider alternative options like balance transfers or personal loans. You can also try again in a few months, especially if your credit score improves.

Conclusion

Alright, friends, we've reached the end of our journey to conquer those pesky credit card interest rates. We've armed you with the knowledge and strategies you need to negotiate like a pro and unlock significant savings. Remember, securing a lower interest rate is all about knowing your worth, doing your research, and being confident and persistent in your approach. You've learned how to assess your credit score, research current market trends, craft a compelling pitch, and navigate the negotiation process with poise and determination. We've also discussed alternative options like balance transfers and personal loans, ensuring you have a comprehensive toolkit to tackle high interest rates head-on.

Now it's your turn to take action! Pick up the phone, contact your credit card company, and put these strategies to the test. Don't let those high interest rates continue to eat away at your hard-earned money. Remember, every dollar you save on interest is a dollar you can put towards your financial goals, whether it's paying off debt, saving for a down payment on a house, or simply enjoying a little extra financial freedom.

So, are you ready to take control of your finances and say goodbye to unnecessary interest payments? Go for it – you've got this!