Weathering the Storm: Building Your Ultimate Emergency Fund

Hey there, friends! Let's talk about something that might not be the most thrilling topic, but trust me, it's as essential as that first cup of coffee in the morning – building an emergency fund. I know, I know, saving money can feel like watching paint dry sometimes, especially when there are so many shiny things calling our names (hello, new gadget!). But think of your emergency fund as your financial superhero cape. It's there to swoop in and save the day when unexpected chaos hits.

We've all been there, right? One minute you're cruising along, feeling financially savvy, and the next, BAM! Your car decides to impersonate a boat (leaky radiator, anyone?), your fridge throws a tantrum and stops chilling (goodbye, groceries!), or worse, you're facing an unexpected job loss. Life, as they say, loves to throw curveballs when you least expect it. And guess what? Those curveballs almost always come with a price tag.

Now, imagine facing those situations without a financial safety net. The stress! The panic! The instant ramen dinners for the next month! It's enough to make anyone break out in a cold sweat. But here’s the good news: building an emergency fund doesn't have to be a Herculean task. It's about small, consistent steps that gradually create a cushion against life's inevitable bumps. Think of it as building a fortress, brick by brick, against financial storms.

Perhaps you're thinking, "I'm living paycheck to paycheck, how can I possibly save anything?" Or maybe you're tempted to skip saving altogether, thinking, "I'll just put it on a credit card!" (Trust me, future you will not thank you for that). I understand! We’ve all been in those tight spots. But the truth is, even small contributions can make a huge difference over time. It's like planting a tiny seed that eventually grows into a mighty oak tree.

So, are you ready to learn how to build your own financial fortress? Are you ready to say goodbye to financial panic and hello to peace of mind? This guide is your roadmap to creating an emergency fund that will protect you from life’s curveballs. We'll break down the process into manageable steps, explore different savings strategies, and even tackle some common misconceptions about emergency funds. Get ready to transform your financial life, one small step at a time. Stick around, and let's get started!

The Ultimate Guide to Building an Emergency Fund: Why it Matters

Let's dive deep into the world of emergency funds. We'll explore why they're so crucial, how to determine the right amount for you, and the best strategies to build one, even if you're starting from scratch. This isn't just about saving money; it's about creating a sense of security and control in a world that often feels unpredictable.

Why You Absolutely, Positively Need an Emergency Fund

Okay, let's get real. Why bother with an emergency fund? It's simple: life happens. And sometimes, life happens in the form of unexpected expenses that can throw your entire financial stability into disarray. Without an emergency fund, you're essentially walking a financial tightrope without a safety net.

• The Unexpected Will Happen

It's not a matter of if, but when. Your car will break down, your water heater will burst, you'll need to pay for a medical emergency, or you might face job loss. These are all real-life scenarios that can derail your finances if you're not prepared. According to a recent study, nearly 60% of Americans couldn't cover a $1,000 emergency with their savings. That's a scary statistic!

• Avoiding Debt Traps

Without an emergency fund, the natural inclination is to turn to credit cards or loans when an unexpected expense arises. This can quickly lead to a debt spiral, where you're paying interest on top of interest, making it even harder to get back on your feet. An emergency fund allows you to avoid these costly traps and maintain control of your finances.

• Peace of Mind

This is perhaps the most underrated benefit. Knowing that you have a financial cushion to fall back on can significantly reduce stress and anxiety. It allows you to sleep better at night, knowing that you're prepared for whatever life throws your way. It's like having a financial security blanket – comforting and reassuring.

• Opportunity Knocks

Sometimes, emergencies aren't just about problems; they can also present opportunities. Imagine you suddenly find the perfect investment opportunity, but you don't have the cash on hand. An emergency fund can provide the funds you need to seize those opportunities and potentially improve your financial situation.

How Much Should You Save? Finding Your Magic Number

This is the million-dollar question (or rather, the "how many months of expenses" question). The generally accepted rule of thumb is to save 3-6 months' worth of living expenses. But let's break that down and personalize it to your situation.

• Calculate Your Monthly Expenses

Start by tracking your monthly expenses. This includes everything from rent or mortgage payments to groceries, utilities, transportation, insurance, and debt payments. Use a budgeting app, spreadsheet, or even a good old-fashioned notebook to keep track of your spending for a month or two. Be honest with yourself – don't forget those "fun" expenses like entertainment and dining out.

• Assess Your Risk Tolerance

Are you a naturally cautious person? Do you work in a stable industry? Or are you more of a risk-taker with a job that's prone to fluctuations? Your risk tolerance will influence how much you need to save. If you're in a stable job and have minimal debt, you might be comfortable with 3 months' worth of expenses. But if you're self-employed or work in a volatile industry, 6 months or even more might be a better target.

• Consider Your Family Situation

Do you have dependents? A family to support? These factors will also influence the amount you need to save. If you're the sole provider for your family, you'll need a larger emergency fund to cover their needs in case of job loss or other unexpected events.

• Factor in Potential Unexpected Costs

Think about potential unexpected costs that you might face. Do you have an older car that's likely to need repairs? Are you planning any major home renovations? Factor these potential costs into your emergency fund target.

• Start Small, Adjust as Needed

Don't get overwhelmed by the thought of saving 3-6 months' worth of expenses. Start small and gradually increase your savings over time. As your income and expenses change, adjust your emergency fund target accordingly.

Building Your Emergency Fund: Practical Strategies That Work

Now for the fun part: actually building your emergency fund! Here are some practical strategies that can help you reach your savings goals.

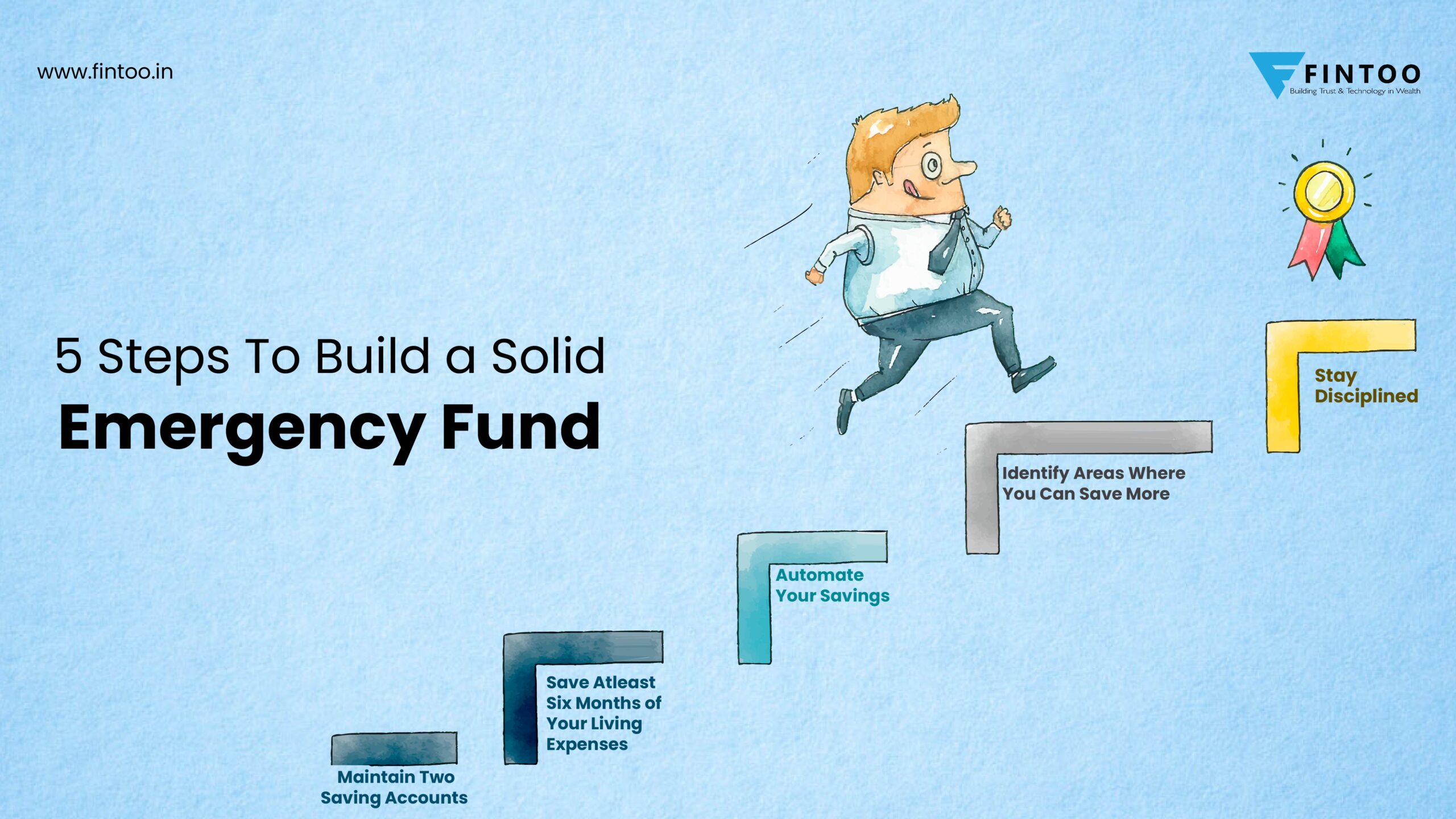

• Automate Your Savings

This is the single most effective strategy for building an emergency fund. Set up automatic transfers from your checking account to your savings account each month. Treat it like a bill payment – something that happens automatically without you having to think about it. Even small amounts, like $25 or $50 per month, can add up significantly over time.

• Cut Unnecessary Expenses

Take a close look at your spending and identify areas where you can cut back. Do you really need that daily latte? Can you cancel that unused gym membership? Can you cook more meals at home instead of eating out? Small changes can have a big impact on your savings.

• The "Spare Change" Strategy

Round up your purchases to the nearest dollar and transfer the difference to your savings account. There are apps that can automate this process, making it even easier. You'd be surprised how quickly those spare cents add up!

• The "Windfall" Strategy

Whenever you receive a windfall – a bonus, a tax refund, a gift – put a portion of it directly into your emergency fund. This is a great way to accelerate your savings progress.

• The "Side Hustle" Strategy

Consider starting a side hustle to earn extra income. This could be anything from freelancing to driving for a ride-sharing service to selling crafts online. The extra income can be used to quickly build your emergency fund.

• The "No Spend" Challenge

Challenge yourself to a "no spend" week or month. During this time, avoid all non-essential purchases. This can help you identify areas where you're overspending and free up more money for your emergency fund.

Where to Keep Your Emergency Fund: Accessibility vs. Growth

Choosing the right place to store your emergency fund is crucial. You want it to be easily accessible in case of an emergency, but you also want it to earn some interest.

• High-Yield Savings Account

This is generally the best option for an emergency fund. High-yield savings accounts offer competitive interest rates while still providing easy access to your funds. Look for accounts that are FDIC-insured for added security.

• Money Market Account

Money market accounts are similar to savings accounts, but they may offer slightly higher interest rates. However, they may also have minimum balance requirements or restrictions on withdrawals.

• Certificate of Deposit (CD) Ladder

While CDs typically lock up your money for a set period, a CD ladder can provide some flexibility. This involves investing in multiple CDs with staggered maturity dates, so you have access to some of your funds every few months.

• Avoid Risky Investments

Your emergency fund should not be invested in the stock market or other risky assets. The goal is to preserve your capital, not to generate high returns. The risk of losing money is simply too high for funds that you might need in an emergency.

Common Emergency Fund Mistakes to Avoid

Building an emergency fund is a journey, and it's easy to make mistakes along the way. Here are some common pitfalls to avoid.

• Not Having One At All

This is the biggest mistake of all. As we've discussed, an emergency fund is essential for financial security and peace of mind.

• Using It For Non-Emergencies

It's tempting to dip into your emergency fund for non-essential purchases, but resist the urge. An emergency fund is for true emergencies only – unexpected expenses that you couldn't have planned for.

• Not Replenishing It After Use

If you do have to use your emergency fund, make it a priority to replenish it as soon as possible. Treat it like a revolving line of credit that needs to be paid back after each use.

• Keeping It Too Accessible

While you want your emergency fund to be easily accessible, you don't want it to be too accessible. If it's too easy to withdraw funds, you're more likely to use it for non-emergencies. Consider keeping it in a separate account that requires a few extra steps to access.

• Thinking It's a One-Time Effort

Building an emergency fund is not a one-time effort. It's an ongoing process that requires regular maintenance and adjustments. As your income and expenses change, you'll need to adjust your savings goals accordingly.

Building an emergency fund is a powerful step towards financial security. It’s not always easy, but it’s always worth it. By automating your savings, cutting unnecessary expenses, and choosing the right place to store your funds, you can create a financial safety net that will protect you from life’s inevitable curveballs.

Emergency Fund FAQs

Let's tackle some frequently asked questions about emergency funds to clarify any lingering doubts and provide further guidance.

• Q: Is an emergency fund the same as a retirement fund?

• A: No, absolutely not! An emergency fund is for short-term, unexpected expenses, while a retirement fund is for long-term financial security during your retirement years. Don't raid your retirement savings for emergencies, as this can have serious consequences for your future.

• Q: What if I have debt? Should I focus on paying that off first?

• A: It's a common dilemma. The general advice is to build a small emergency fund of $1,000 before aggressively paying down debt. This will prevent you from racking up more debt when an emergency arises. Once you have that small cushion, focus on paying off high-interest debt, then resume building your emergency fund to the recommended 3-6 months of expenses.

• Q: What if I'm self-employed or have an irregular income?

• A: If you have an irregular income, it's even more crucial to have a robust emergency fund. Aim for the higher end of the 3-6 month range, or even more if you can. Track your income and expenses carefully to identify trends and plan accordingly.

• Q: What if I have multiple savings goals, like a down payment on a house or a vacation?

• A: Prioritize your emergency fund first. It's the foundation of your financial security. Once you have a solid emergency fund in place, you can then focus on other savings goals. Consider setting up separate savings accounts for each goal to keep your finances organized.

Building an emergency fund is a journey, and it's perfectly normal to have questions along the way. Don't be afraid to seek advice from financial professionals or trusted friends and family members. The most important thing is to start somewhere and stay consistent with your savings efforts.

So, there you have it – the ultimate guide to building an emergency fund! We've covered why it matters, how much you should save, practical strategies to build it, where to keep it, common mistakes to avoid, and frequently asked questions. It might seem daunting at first, but remember, it's about taking small, consistent steps. Each dollar you save is a step closer to financial security and peace of mind.

Now, it's time to take action. Start by calculating your monthly expenses and setting a savings goal. Automate your savings, cut unnecessary expenses, and find a high-yield savings account to store your funds. Remember, every little bit counts!

I challenge you to take one small step towards building your emergency fund today. It could be as simple as setting up an automatic transfer for $25 per month or skipping that expensive coffee tomorrow. The important thing is to get started. You've got this! What small step will you take today to secure your financial future?